S&P ratings are an essential aspect of the financial world, providing investors and stakeholders with a measure of creditworthiness for various entities, including corporations, governments, and financial instruments. Standard & Poor's (S&P) is a renowned global credit rating agency that evaluates and assigns ratings based on a rigorous assessment of financial health and credit risk. These ratings play a crucial role in investment decisions, influencing interest rates, market confidence, and economic stability. Understanding the intricacies of S&P ratings can empower investors and financial professionals to make informed choices and mitigate risk in an ever-evolving market landscape.

The significance of S&P ratings extends beyond the financial markets, affecting the broader economy and influencing policy decisions. As a trusted source of credit analysis, S&P ratings provide a standardized framework for assessing credit risk, enabling comparability across different entities and financial products. This standardized approach facilitates transparency and consistency, fostering confidence among investors and stakeholders. Moreover, S&P ratings are often used as benchmarks for regulatory purposes, guiding capital requirements and risk management practices for financial institutions.

In this comprehensive guide, we will explore the various facets of S&P ratings, from their historical development and methodology to their impact on markets and economies. We will delve into the different types of credit ratings, their criteria, and the factors influencing them. Additionally, we will address common questions and misconceptions about S&P ratings, providing a clear and concise understanding of their role and significance. Whether you are an investor, financial professional, or simply curious about credit ratings, this guide offers valuable insights to enhance your knowledge and decision-making capabilities.

Read also:Mastering The Art Of Performance Auto Body Techniques And Innovations

Table of Contents

- What are S&P Ratings?

- History of S&P Ratings

- How Are S&P Ratings Determined?

- Types of S&P Ratings

- Importance of S&P Ratings

- Methodology Behind S&P Ratings

- Factors Influencing S&P Ratings

- Impact of S&P Ratings on Markets

- S&P Ratings and Economic Stability

- S&P Ratings vs. Other Rating Agencies

- Common Misconceptions About S&P Ratings

- How to Interpret S&P Ratings?

- Frequently Asked Questions

- Conclusion

What are S&P Ratings?

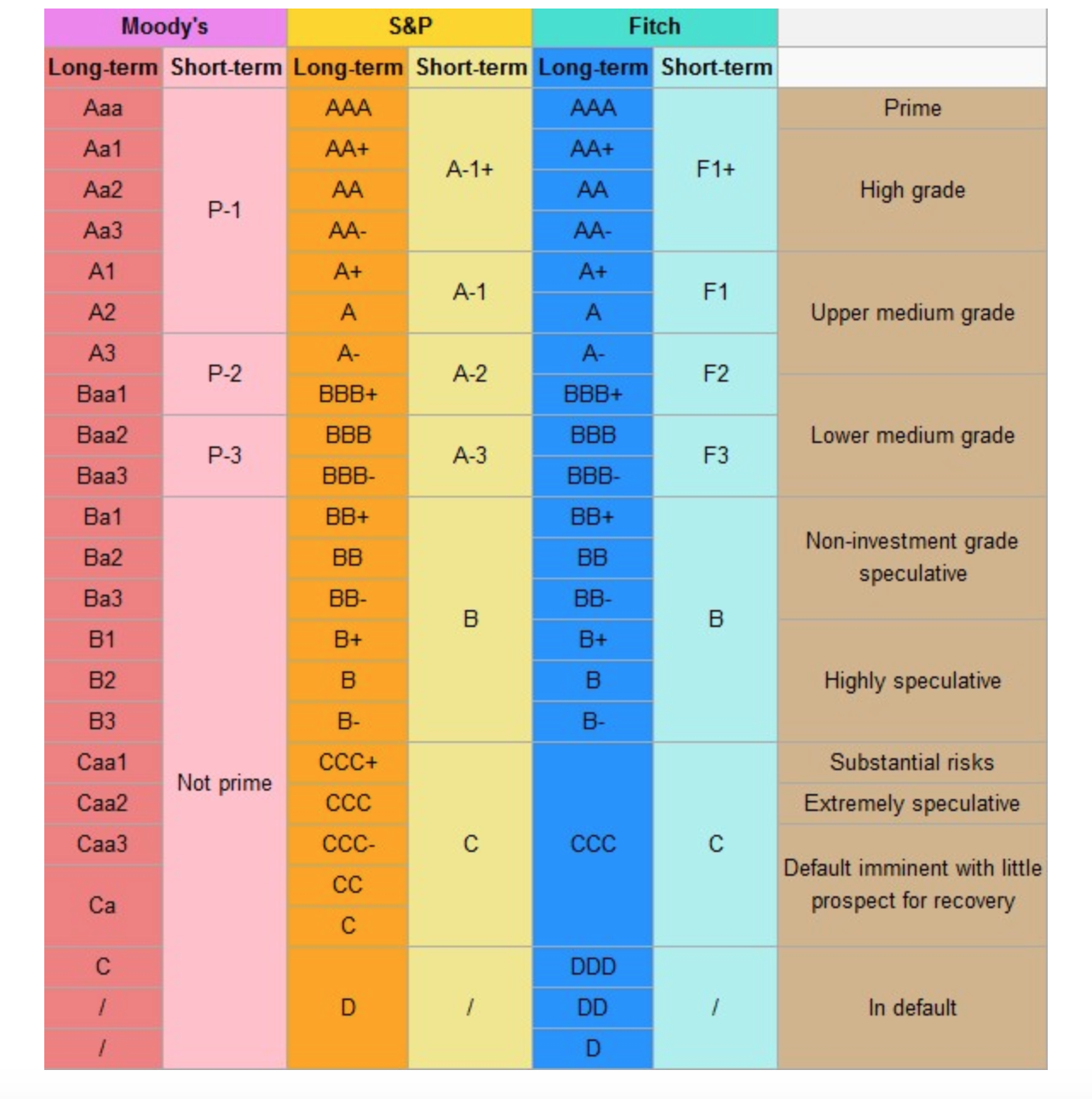

S&P ratings, issued by Standard & Poor's, are evaluations of the creditworthiness of entities such as corporations, governments, and financial instruments. These ratings provide insights into the likelihood of an entity meeting its financial obligations, offering a standardized measure of credit risk for investors and stakeholders. S&P ratings range from 'AAA', the highest credit quality, to 'D', indicating default, with various gradations in between to reflect differing levels of creditworthiness.

History of S&P Ratings

The history of S&P ratings dates back to the early 20th century when Standard Statistics merged with Poor's Publishing to form Standard & Poor's. Initially, the company focused on providing financial information and analysis to investors. Over the years, S&P evolved into a leading credit rating agency, establishing a reputation for its rigorous and objective assessment of credit risk. Today, S&P is part of S&P Global, a financial services company known for its comprehensive financial research and analysis.

How Are S&P Ratings Determined?

S&P ratings are determined through a comprehensive analysis of an entity's financial health, market position, and credit risk. The process involves a detailed examination of financial statements, management quality, industry conditions, and macroeconomic factors. S&P employs a team of analysts who conduct qualitative and quantitative assessments to arrive at a credit rating that reflects the entity's ability to meet its obligations. The rating is subject to regular review and can be adjusted based on changes in the entity's financial condition or external environment.

Types of S&P Ratings

S&P offers several types of credit ratings, each serving a specific purpose. These include:

- Issuer Credit Ratings: These ratings assess the creditworthiness of entities such as corporations and governments.

- Issue Credit Ratings: These ratings evaluate the credit risk associated with specific financial instruments, such as bonds.

- Short-Term Ratings: These ratings focus on the credit risk of obligations with a maturity of less than one year.

- Long-Term Ratings: These ratings assess the creditworthiness of obligations with a maturity of more than one year.

Importance of S&P Ratings

S&P ratings play a vital role in the financial markets by providing a standardized measure of credit risk. They influence investment decisions, interest rates, and market confidence, serving as a benchmark for assessing the creditworthiness of entities and financial products. S&P ratings also impact regulatory requirements, guiding capital adequacy and risk management practices for financial institutions. By offering a transparent and consistent framework for credit analysis, S&P ratings enhance market efficiency and economic stability.

Methodology Behind S&P Ratings

The methodology behind S&P ratings involves a thorough analysis of various factors that influence an entity's creditworthiness. These factors include:

Read also:Jerome Flynn A Talented Actor With A Unique Path In Entertainment

- Financial Performance: An assessment of the entity's revenue, profitability, cash flow, and debt levels.

- Business Risk Profile: An evaluation of the entity's industry position, competitive advantage, and market conditions.

- Management Quality: An analysis of the entity's leadership, governance practices, and strategic direction.

- Economic Environment: A consideration of macroeconomic factors, such as interest rates, inflation, and economic growth.

Factors Influencing S&P Ratings

Several factors can influence S&P ratings, including:

- Financial Health: An entity's financial stability, liquidity, and debt levels play a crucial role in determining its credit rating.

- Market Conditions: Industry trends, competitive dynamics, and economic conditions can impact an entity's creditworthiness.

- Regulatory Environment: Changes in regulations and compliance requirements can affect an entity's financial position and credit risk.

- External Shocks: Unforeseen events, such as natural disasters or geopolitical tensions, can influence an entity's credit rating.

Impact of S&P Ratings on Markets

S&P ratings have a significant impact on financial markets, shaping investor behavior and influencing market dynamics. A change in an entity's S&P rating can affect its borrowing costs, access to capital, and overall market confidence. A downgrade in an S&P rating may lead to higher interest rates and reduced investor interest, while an upgrade can enhance market perception and attract investment. Moreover, S&P ratings are often used as benchmarks for pricing financial instruments and assessing risk in investment portfolios.

S&P Ratings and Economic Stability

S&P ratings contribute to economic stability by providing a reliable measure of credit risk and fostering transparency in financial markets. By enabling investors and stakeholders to assess creditworthiness, S&P ratings help maintain market confidence and support efficient capital allocation. Additionally, S&P ratings guide regulatory frameworks and risk management practices, promoting financial stability and mitigating systemic risk. Through their role in credit analysis, S&P ratings play a critical part in ensuring the resilience of financial systems and economies.

S&P Ratings vs. Other Rating Agencies

S&P ratings are often compared to those issued by other prominent credit rating agencies, such as Moody's and Fitch Ratings. While all these agencies provide credit assessments, there are differences in their methodologies, rating scales, and criteria. S&P is known for its rigorous analysis and comprehensive approach, focusing on both qualitative and quantitative factors. Despite these differences, S&P, Moody's, and Fitch are collectively recognized as the "Big Three" rating agencies, with their ratings widely used by investors, regulators, and financial institutions.

Common Misconceptions About S&P Ratings

There are several misconceptions about S&P ratings that can lead to confusion among investors and stakeholders. Some common myths include:

- S&P Ratings Predict Defaults: While S&P ratings assess credit risk, they do not predict specific defaults or financial outcomes.

- All Entities with the Same Rating Have Equal Risk: Ratings provide a relative measure of credit risk, but entities with the same rating may still have different risk profiles.

- S&P Ratings Remain Constant: Ratings are subject to regular review and can change based on an entity's financial condition or external environment.

How to Interpret S&P Ratings?

Interpreting S&P ratings requires an understanding of the rating scale and what each rating signifies. The ratings range from 'AAA', indicating the highest credit quality, to 'D', representing default. Each rating reflects a level of creditworthiness and associated risk, helping investors gauge the likelihood of an entity meeting its financial obligations. It's important to consider the context of the rating, including the entity's financial health, market conditions, and external factors, to make informed investment decisions.

Frequently Asked Questions

Here are some common questions about S&P ratings:

- What is the highest S&P rating? The highest S&P rating is 'AAA', indicating the highest level of creditworthiness.

- How often are S&P ratings reviewed? S&P ratings are regularly reviewed and can be updated based on changes in an entity's financial condition or external environment.

- Do S&P ratings affect interest rates? Yes, S&P ratings can influence interest rates, with higher ratings typically resulting in lower borrowing costs.

- Can S&P ratings change over time? Yes, S&P ratings can change based on an entity's financial health, market conditions, and other factors.

- What is the difference between issuer and issue credit ratings? Issuer credit ratings assess the creditworthiness of an entity, while issue credit ratings evaluate the risk of specific financial instruments.

- Are S&P ratings used for regulatory purposes? Yes, S&P ratings are often used as benchmarks for regulatory purposes, guiding capital requirements and risk management practices.

Conclusion

S&P ratings play a pivotal role in the financial markets, offering a standardized measure of credit risk that influences investment decisions, market confidence, and economic stability. As a trusted source of credit analysis, S&P ratings provide valuable insights into the creditworthiness of entities and financial instruments, empowering investors and stakeholders to make informed choices. By understanding the methodology, factors, and implications of S&P ratings, individuals and organizations can effectively navigate the complex landscape of credit risk and enhance their financial decision-making capabilities.

:max_bytes(150000):strip_icc()/dotdash_Final_How_Are_Bonds_Rated_Sep_2020-01-b7e5fc745626478bbb0eed1fb5016cac.jpg)